For millions of Pakistani families, owning a home has always felt like a distant dream. Rising property prices, expensive construction costs, and high-interest bank loans have kept that dream out of reach for the average citizen for decades. That is now changing.

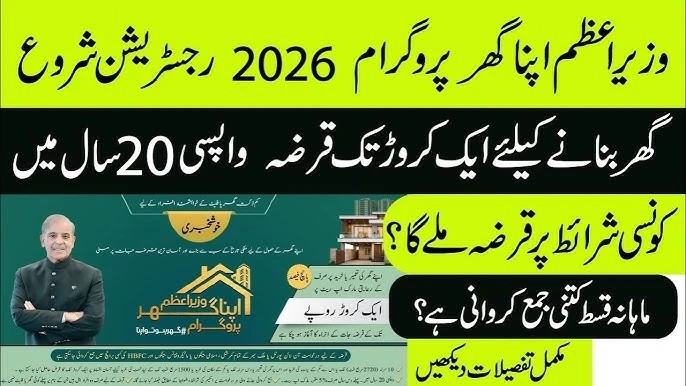

Prime Minister Shehbaz Sharif officially launched the Wazir-e-Azam Apna Ghar Program 2026 — carrying the powerful slogan “Ghar Ho Tu Apna“ (A Home That Is Truly Yours) — on 30 April 2026 in Islamabad. The ceremony was attended by Deputy Prime Minister Ishaq Dar, federal ministers, and senior government officials. Cheques were distributed to successful applicants of the first phase right at the launch event, proving this is not just a promise on paper — it is already delivering results.

This comprehensive guide covers everything you need to know:

- What the PM Apna Ghar Scheme 2026 is

- Who is eligible to apply

- Loan amount, markup rate, and monthly installment breakdown

- Required documents

- Step-by-step online application process

- Participating banks

- Frequently Asked Questions

If you are serious about owning your own home, read this guide carefully — it could be the most important decision you make in 2026.

What Is the PM Apna Ghar Scheme 2026?

The Wazir-e-Azam Apna Ghar Program is a government-backed subsidized housing finance initiative specifically designed for low and middle-income Pakistani families. Its primary goal is to make homeownership accessible to first-time buyers who do not currently own a house anywhere in Pakistan.

The scheme operates on a 90:10 financing model — participating banks cover 90% of the total property value while the applicant contributes only 10% as a down payment. This is combined with a heavily subsidized markup rate of just 5% per annum for the first 10 years, compared to the market rate of 15–22% charged by commercial banks.

This program is the upgraded and improved version of the earlier “Mera Ghar Mera Ashiana“ scheme, relaunched in 2026 with broader eligibility, better terms, and a nationwide digital application system.

Quick Overview Table

| Feature | Details |

|---|---|

| Scheme Name | Wazir-e-Azam Apna Ghar Program |

| Launch Date | 30 April 2026 |

| Official Website | apnaghar.gov.pk |

| Maximum Loan | Rs. 10,000,000 (1 Crore) |

| Minimum Loan | Rs. 2,500,000 (25 Lakh) |

| Markup Rate | 5% Fixed (First 10 Years) |

| Loan Tenure | Up to 20 Years |

| Government Financing | 90% of Property Value |

| Applicant Contribution | 10% Down Payment |

| Processing Fee | None (Zero) |

| Prepayment Penalty | None |

| Coverage | All 4 Provinces + GB + AJK |

| Year 1 Target | 50,000 Houses |

Eligibility Criteria — Who Can Apply?

Before filling out any form, Prime Minister Apna Ghar Scheme Online Apply confirm that you meet the eligibility requirements. Applying without qualifying is the most common reason for rejection and wasted effort.

1. Pakistani Citizenship

You must be a Pakistani citizen with a valid CNIC. Overseas Pakistanis holding a NICOP are also eligible to apply under this scheme.

2. First-Time Homebuyer

This scheme is exclusively for people who do not already own a home. If you have a house, flat, or any residential property registered in your name anywhere in Pakistan, you are not eligible. This condition is verified through NADRA records.

3. Age Requirement

Applicants must be between 21 and 60 years of age. The bank will calculate the loan tenure so that the final repayment falls before the applicant reaches retirement age. For example, if you are 55 years old, you may only qualify for a 5-year tenure.

4. Stable Source of Income

You must have a regular and verifiable income. The scheme is open to:

- Salaried individuals (government or private sector)

- Self-employed persons and business owners

- Freelancers (provable through consistent bank statements)

- Informal income earners (bank statement showing regular transactions is acceptable)

5. No Bank Default History

You must not be a defaulter of any bank or financial institution. Participating banks will check your credit history through the State Bank of Pakistan’s credit bureau. If you have a default, clear it before applying.

6. Property Size Requirements

The loan facility can be used for:

- Purchase of a plot up to 10 Marla

- Purchase of a constructed house up to 10 Marla

- Purchase of a flat up to 1,500 square feet

- Construction of a home on land you already own

7. Debt-to-Income Ratio

Banks will evaluate whether your monthly installment is affordable relative to your monthly income. The installment should not exceed a specified percentage of your earnings, ensuring you are not financially over-burdened.

Loan Amount and Monthly Installment Breakdown

The scheme offers financing from Rs. 25 Lakh up to Rs. 1 Crore. Below is a clear breakdown of estimated monthly installments based on a 5% markup rate over a 20-year tenure:

| Loan Amount | Approximate Monthly Installment |

|---|---|

| Rs. 2,500,000 (25 Lakh) | Rs. 16,499 |

| Rs. 5,000,000 (50 Lakh) | Rs. 32,997 |

| Rs. 7,500,000 (75 Lakh) | Rs. 49,497 |

| Rs. 10,000,000 (1 Crore) | Rs. 65,990 |

Figures based on 5% fixed markup and 20-year repayment period.

Markup Rate Structure

- Years 1–10: 5% fixed markup rate (government-subsidized)

- Years 11–20: Market-based or prevailing markup rate applies

This structure means your monthly payment is locked and predictable for the first decade — giving you financial stability when you need it most.

Understanding the Down Payment

The 90:10 model is genuinely one of the best deals ever offered in Pakistan’s housing sector. Here is how it works in practice:

- If you want to buy or build a Rs. 50 Lakh home

- You contribute only Rs. 5 Lakh (10%) from your pocket

- The government and bank together cover Rs. 45 Lakh (90%)

- You repay the Rs. 45 Lakh over up to 20 years at a subsidized rate

For the first time in Pakistan’s history, this combination of low down payment, long tenure, and subsidized markup is available at this scale.

Required Documents — Complete Checklist

Prepare these documents before you start filling out the application form. Missing even one document can delay or reject your application.

Personal Documents (Required for All Applicants)

- CNIC — original, front and back (and family members’ CNICs if relevant)

- Proof of Income:

- Salaried employees: Last 3 months’ salary slips + employment letter

- Self-employed: Business registration documents or 6-month bank statement

- Freelancers: 6-month bank statement showing regular income deposits

- Bank Statement — last 6 months from your primary account

- Recent Utility Bill — electricity or gas bill as proof of current address

- Passport-size Photographs — 2 to 4 recent photos with blue or white background

Property Documents (If You Own Land)

- Fard or Registry — land ownership proof

- Allotment Letter — if the plot is in a housing scheme

- Possession Document — proving physical ownership of the land

- Building Plan or Site Map — if applying for a construction loan

Additional Documents

- Affidavit — a signed declaration confirming you do not own any other property (template is available on the portal)

- Tax Return or NTN — if applicable

- Co-applicant’s CNIC — if applying jointly with a spouse or sibling

Important Tip:

Scan all documents as PDF or high-quality JPG. Keep each file under 2MB. Blurry, incomplete, or cut-off documents are rejected without notice. Use a proper scanner or a well-lit phone camera.

How to Apply Online — Step-by-Step Guide

The entire application process can be completed from home. Here is exactly how to do it:

Step 1: Visit the Official Website

Open your browser and go to apnaghar.gov.pk. This is the only official federal portal. Do not trust any other website or agent claiming to help you apply.

Step 2: Create Your Account

- Click the “Register” or “Create Account” button

- Enter your CNIC number

- Enter your verified mobile number — an OTP (One-Time Password) will be sent to it

- Enter the OTP to verify your account

- Set a strong password

Step 3: Log In

Use your CNIC number and password to log into your account.

Step 4: Fill in the Application Form

Complete all sections of the form carefully:

- Personal Details: Full name, date of birth, current and permanent address

- Family Information: Number of dependents

- Income Details: Source of income and monthly amount

- Property Details: What you want to purchase or build (type, location, size)

- Loan Details: How much financing you need and preferred repayment period

- Bank Preference: Choose from the list of participating banks

Step 5: Upload Documents

Upload each required document in the appropriate section of the form. Do not skip any required document even if you think it may not apply to you.

Step 6: Review Before Submitting

Double-check every piece of information before hitting submit. Providing incorrect information does not just get your application rejected — it can create serious legal complications later.

Step 7: Submit and Save Your Tracking ID

Click “Submit.” You will receive a unique Application Reference Number or Tracking ID. Save this as a screenshot or write it down — you will need it to track your application status.

Step 8: Wait for Bank Contact

After submission, your selected bank will contact you within 15 days. The government has officially directed all participating banks to complete approvals within this timeframe.

Step 9: Bank Verification Visit

You will need to visit the bank branch for:

- Document verification

- Property valuation (for properties up to Rs. 5 million, banks conduct their own valuation; above Rs. 5 million requires a government-approved valuer)

- Final loan offer and signing of agreement

Step 10: Loan Disbursement

Once approved, the loan is disbursed — in phases for construction loans, and in full for ready-property purchases.

How to Check Your Application Status

You can track your application from home using three methods:

Online Portal: Log in to apnaghar.gov.pk and navigate to the “Application Status” section using your Tracking ID.

SMS Updates: Your registered mobile number will receive automatic updates at key stages of the process.

Helpline: Call the official helpline number listed on the portal for real-time assistance.

Participating Banks and Financial Institutions

The following banks and institutions are part of the PM Apna Ghar Scheme 2026:

- HBL (Habib Bank Limited)

- UBL (United Bank Limited)

- NBP (National Bank of Pakistan)

- Bank AL Habib

- Allied Bank Limited

- Meezan Bank (Islamic/Shariah-compliant option)

- House Building Finance Company (HBFC)

- Microfinance Institutions (for smaller loan amounts)

Choosing Your Bank:

Each bank offers slightly different processing times and customer support quality. You can choose your preferred bank during the application process. For those seeking Shariah-compliant financing, Meezan Bank and other Islamic banks offer housing finance under the Diminishing Musharakah model.

Three Ways to Use Your Loan

Option 1: Buy a Plot and Build

If you do not own land, you can use the loan to first purchase a plot and then construct your home on it. The scheme covers both stages.

Option 2: Buy a Ready-Made House or Flat

Looking to purchase an already-built property? The scheme covers this as well — residential houses up to 10 Marla or flats up to 1,500 square feet.

Option 3: Construction on Your Own Land

Already own a plot? You can apply for a construction-only loan to build on your existing land without needing to purchase property.

Federal vs. Punjab Housing Scheme — Key Differences

Alongside the federal PM Apna Ghar Scheme, Punjab is running a separate initiative called “Apni Chhat Apna Ghar” under Chief Minister Maryam Nawaz. Here is how the two compare:

| Feature | PM Apna Ghar (Federal) | Apni Chhat Apna Ghar (Punjab) |

|---|---|---|

| Markup Rate | 5% (first 10 years) | 0% (completely interest-free) |

| Maximum Loan | Rs. 1 Crore | Rs. 15 Lakh |

| Coverage | All Pakistan | Punjab Only |

| Official Website | apnaghar.gov.pk | acag.punjab.gov.pk |

| Monthly Installment | Rs. 16,499–65,990 | Rs. 14,000–26,000 |

| Target Beneficiaries | Middle class | Low income families |

| PMT Score Requirement | Not required | Below 60 in NSER |

| Helpline | Portal helpline | 0800-09100 |

If you live in Punjab and fall in the low-income bracket, the Punjab scheme with its zero markup is worth exploring. If you need a larger loan amount or live outside Punjab, the federal PM Apna Ghar Scheme is the right choice.

Key Benefits of the PM Apna Ghar Scheme

90% Government Financing

You only need to arrange 10% yourself. The rest is covered — reducing the financial barrier to homeownership dramatically.

Historically Low Markup Rate

At 5%, this is far below the 15–22% commercial bank rates. Over 20 years, this saves you an enormous amount.

Zero Processing Fees

There are no application charges, no processing fees, and no hidden costs. The scheme is completely free to apply for.

No Prepayment Penalty

If you come into money and want to pay off your loan early, you are free to do so with no extra charges.

20-Year Repayment Tenure

Spread your repayment over two decades, keeping monthly installments manageable even on a modest income.

Nationwide Availability

Open to citizens from all four provinces, Gilgit-Baltistan, and Azad Jammu & Kashmir — not limited to any specific region.

Freelancers and Informal Workers Welcome

Unlike traditional bank loans, this scheme has a dedicated option for freelancers and informal income earners.

Co-Applicant Option

Apply with your spouse or sibling as a co-applicant. Combined income can increase your eligible loan amount significantly.

Fraud Warning — Protect Yourself ⚠️

The government has made it crystal clear: this scheme has absolutely zero fees. If any agent, middleman, or website asks you to pay money to submit your application or help you get approved — do not pay. That is fraud.

Stay safe by following these rules:

- Only apply through apnaghar.gov.pk or your bank’s official website

- Never share your CNIC number or OTP with anyone

- Never pay any unofficial agent or third party

- If someone attempts to defraud you, report it at cybercrime.gov.pk

Thousands of scammers operate around legitimate government schemes. Stay alert and trust only official sources.

Frequently Asked Questions (FAQ)

Conclusion — Your Dream Home Is Within Reach

The Wazir-e-Azam Apna Ghar Program 2026 is a landmark initiative in Pakistan’s housing sector. The combination of 90% government financing, a 5% subsidized markup rate, zero fees, no prepayment penalty, and a 20-year repayment period has simply never been available at this scale before. The government’s first-year target of 50,000 homes shows the ambition and seriousness behind this program.

If you have been renting for years, struggling to save for a down payment, or simply watching property prices rise faster than your savings — this scheme is built for you. Whether you are a salaried professional, a small business owner, a freelancer, or someone with informal income, there is a path for you in this program.

Take action today. Gather your documents, visit apnaghar.gov.pk, and take the first real step toward owning a home you can call your own.